grenke around the globe

grenke around the globe

Please note that this website shows an excerpt from the grenke AG Annual Report 2025. The annual report, which is also available in the “Reports & Key Figures” section of the grenke AG website, prevails.

Current risk environment

The ongoing geopolitical crises and conflicts continue to create significant uncertainty on the future course of the macroeconomies in the different core markets of the grenke Group. Potentially escalating trade conflicts may have short-term adverse effects on global supply chains and significantly weigh on global economic growth. Increasing trade restrictions, such as changes in U.S. tariff policy, materially affect economic growth, particularly in highly export-oriented countries such as Germany. In this environment, grenke is monitoring the risk developments in its core business – the lease portfolio – with a particular focus on individual sectors that may be especially affected, despite the continued high level of diversification.

The persistent geopolitical tensions, particularly in the Middle East and the war in Ukraine, are leading to greater fluctuations in energy prices, intensifying inflationary pressures, and contributing to increased volatility in the capital markets.

All risks that are identified are systematically recognised, assessed, monitored, and managed within the framework of the Group-wide risk management system. The key elements of the grenke Group’s risk management system, as well as the relevant risk categories and their management, are explained in greater detail below.

Principles of risk management

Drawing on many years of experience, the grenke Group has developed and implemented a comprehensive risk management system. This system is continuously refined and complies with the requirements of the German Stock Corporation Act (Aktiengesetz) as well as all relevant statutory and regulatory provisions. Risk management at the grenke Group is an integral part of the corporate strategy and is designed to ensure long-term, sustainable, and successful business operations.

This includes, particularly, profitable and sustainable growth, ensuring a continuous and appropriate dividend payout, and maintaining the Company’s financial stability. Regular profit retention appropriately strengthens equity. Investments in personnel and technological resources safeguard the grenke Group's future viability.

A key guiding principle of our risk management is to maintain a balance between pursuing earnings opportunities and assuming risks in a controlled manner. We consistently adhere to the philosophy of taking on only those risks that are necessary and inseparably linked to our business model. We use proprietary statistical models to assess and measure these risks. The objective is not to minimise risks per se, but rather to ensure a high level of forecasting accuracy in our models in order to quantify risks precisely at contract inception and, ideally, to price them appropriately.

We seek to largely avoid market price risks in general – and maturity transformation risk in particular – as well as liquidity risks, or to minimise them through appropriate hedging transactions. Consistent and broad diversification limits concentration risk. The high level of diversification stems in particular from our very broad customer portfolio of more than 716,000 customers in 31 countries, a broad and dynamic asset portfolio, more than 34,500 specialist reseller partners, and various refinancing instruments. This comprehensive diversification lies at the heart of our business model and forms a key foundation of our resilience.

In addition to the intrinsic fundamental principles of our risk culture, which arise from our entrepreneurial conviction and sense of responsibility, we comply with the statutory and regulatory requirements applicable to our risk management as a financial holding company together with our subsidiary, grenke Bank AG.

Risk management system

grenke Group’s risk management system follows a holistic and integrated approach. It comprises all measures for identifying, assessing, evaluating, monitoring, and managing risks arising from the business. In doing so, it considers all relevant Group units and is designed to capture all material individual risks as well as potential risk concentrations and interdependencies among different types of risk. The system’s framework is supported by a deeply embedded and continuously evolving risk culture, as well as by a functional organisational structure with clearly defined responsibilities and processes.

The grenke Group’s risk management system includes the key elements described below, which are generally updated annually. The fundamental orientation of the risk management system is based on the business model defined in the business strategy and the associated strategic business objectives of the Board of Directors.

Business and risk strategy

The fundamental orientation of the risk management system is based on the business model defined in the business strategy and the associated strategic business objectives of the Board of Directors.

In conjunction with the business strategy, the grenke Group risk strategy defines the fundamental risk policy stance, as well as the specifications and objectives of risk management, the determination of risk appetite, and the definition of appropriate measures to achieve the risk-strategic objectives.

Based on the identification of material risks within the framework of the risk inventory, the Risk Appetite Statement, as a key component of the risk strategy, translates the risk-strategic objectives into concrete operational requirements for risk monitoring and management. These quantitative and/or qualitative requirements, in the form of limits and/or thresholds, further specify and operationalise the risk-strategic objectives of the Board of Directors.

Risk inventory

Once a year and, if necessary, on an ad hoc basis, the risks that are material for grenke are identified and assessed by experts in a structured process supported by quantitative metrics.

The key question in this context is which risks could materially affect the capital, earnings or liquidity position of the grenke Group. Particular emphasis is also placed on the systematic identification and assessment of the impacts of ESG risks.

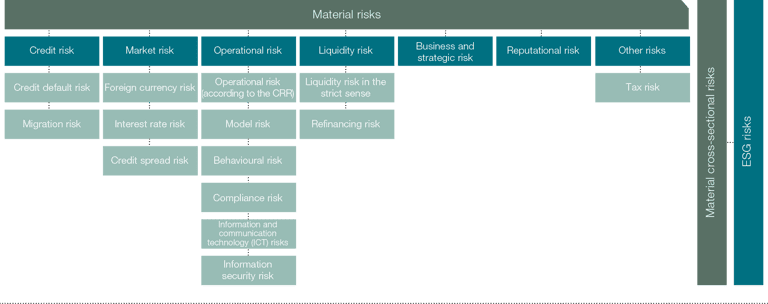

Based on the risk inventory conducted in the financial year 2025, the following risks are material to the grenke Group (aggregated presentation).

Risks assessed as material within the framework of the risk inventory must therefore be comprehensively and continuously measured, monitored, limited, backed by risk capital and appropriately managed within the risk management system.

Risk-bearing capacity and capital adequacy

To ensure risk-bearing capacity and adequate capitalisation at all times, a continuous review is conducted at Group level within an internal process (Internal Capital Adequacy Assessment Process, ICAAP) to determine the extent to which material risks and potential risk concentrations are covered by available risk capital and whether regulatory capital and liquidity requirements are adequately met for at least the three-year capital planning period.

Risk management structure and responsibilities

Our risk management is organised along the three lines of defence (3LoD) model. The clear functional separation between front office and back office functions is consistently implemented through to the level of responsibility of the Board of Directors.

Overall responsibility for the adequacy and effectiveness of risk management at grenke rests with the full Board of Directors. In addition to adopting the business strategy and the risk strategy, including risk policy guidelines, it resolves on the risk appetite (risk appetite statements) and all material methodological and procedural components of risk management.

The independent risk controlling function in accordance with MaRisk is responsible for the appropriate monitoring and communication of material risks, taking into account the effects of ESG risks.

The operational execution of the risk controlling function is carried out by Corporate Risk Management within the grenke Group. This area also encompasses regulatory reporting, the unit responsible for developing and maintaining quantitative risk models, and the independent validation unit, which reviews the adequacy of the internal risk models.

The Risk Working Group (AK Risiko) is likewise part of the risk management system. It primarily addresses current risk-related matters, the results of the risk inventory, any ad hoc risk reports and new legal developments relating to risk management.

In accordance with MaRisk, grenke has established a compliance function, an Anti-Money Laundering Officer, a Chief Information Security Officer, an Outsourcing Officer and a Data Protection Officer.

The core task of the compliance function is to promote the implementation of effective procedures to ensure adherence to the legal regulations and requirements material to the Group. To this end, it identifies and analyses potential compliance risks, conducts legal monitoring and performs corresponding controls. To ensure compliance with the grenke Code of Conduct, which forms the ethical framework for actions within the Group, the Compliance department designs and operates the Group-wide whistleblowing system, develops training and awareness measures on compliance topics and contributes to the drafting of regulations governing the Group-wide management of compliance risks. The function is also responsible for policies relating to individual core compliance topics, such as the handling of potential conflicts of interest.

Our Anti-Money Laundering Officer monitors and supports compliance with anti-money laundering regulations, including due diligence obligations pursuant to the German Anti-Money Laundering Act. Based on policies aligned with statutory and supervisory requirements, a current Group-wide risk analysis and the use of monitoring and analysis tools, risk-based measures are implemented to prevent grenke from being misused for money laundering, terrorist financing or other criminal offences, thereby also mitigating legal and reputational risks. Compliance with these regulations is a shared responsibility to which all employees contribute within their respective areas of responsibility.

Our Chief Information Security Officer is responsible for all information security matters. Through policies and advisory activities, he ensures transparency regarding defined information security objectives and measures and that their implementation is reviewed and monitored on a regular and event-driven basis. In addition, the Chief Information Security Officer oversees information risk management in coordination with Corporate Risk Management.

Our Outsourcing Officer manages and monitors compliance with statutory and regulatory requirements when activities are outsourced to external companies. In accordance with supervisory requirements, the Group has implemented internal control procedures to manage and monitor the aforementioned risks, based on the structure and processes of the relevant procedures.

Our Data Protection Officer (DPO), together with the organisational unit, ensures compliance with all relevant data protection regulations at grenke. The DPO regularly reports to the Board of Directors on the status of data protection at grenke, specifically assessing whether the relevant processes designed to ensure a high level of protection are effective. This involves reviewing the control system, conducting regular data protection analyses, audits and operational reviews, as well as performing systematic formal risk assessments (e.g. through data protection impact assessments) of processes likely to pose high risks to data subjects, as carried out by the respective specialist departments. It also includes overseeing the continuous training of grenke employees and raising their awareness. The DPO is integrated into the established data breach process managed by the data protection organisation, ensuring a swift response to incidents. Our Data Protection Officer also serves as the central point of contact for the supervisory authority. A risk-oriented and process-independent review of the adequacy and effectiveness of risk management is generally conducted annually by our Internal Audit department.

The ICAAP comprises two management perspectives: the “normative perspective”, which has the primary aim of maintaining the institution as a going concern, and the “economic perspective”, focused on protecting creditors.

Under the normative perspective, risk-bearing capacity is ensured if compliance with regulatory key ratios is secured both in the planning scenario, based on the applicable business plan, and in the currently three adverse scenarios over a three-year planning horizon.

The capital available for risk coverage (“risk coverage potential”) consists primarily of regulatory own funds. On the risk side, credit, market price and operational risks are quantified using regulatory prescribed methods. Relevant management metrics include the Common Equity Tier 1 (CET1) requirement, the Supervisory Review and Evaluation Process (SREP) total capital requirement (Pillar 2 Requirement, P2R), the combined buffer requirement, the supervisory capital recommendation (Pillar 2 Guidance, P2G) and additional supervisory structural requirements, such as the leverage ratio.

Since January 1, 2025, an additional capital recommendation from the banking supervisory authority, known as Pillar 2 Guidance, has applied to the grenke Group.

Alongside the Pillar 2 Requirement (P2R), the Pillar 2 Guidance (P2G) constitutes a second capital expectation, derived as standard within the SREP framework but determined individually for each institution, with only the P2R representing a legally binding capital requirement. The P2G represents an extension of the capital conservation buffer concept, i.e. it serves to safeguard the assets of the grenke Group even during periods of stress and may accordingly be offset against the capital conservation buffer. The current level of the P2G for the grenke Group is determined by the results of the regular supervisory stress tests conducted for grenke Bank as a less significant institution (LSI).

Under the economic perspective of the ICAAP, the risk coverage potential is determined and the material risks are quantified on an econom-

ic basis, i.e. on a present value basis. For risk control purposes, the risk coverage potential is then allocated to the material risk types in the form of defined risk limits. In calculating risk, grenke pursues a conservative approach, as also expected by the supervisory authorities, to ensure that rare or extreme events are appropriately taken into account and safeguarded within management (limitation). Under the economic perspective, stress tests for the material risks are calculated on a quarterly basis in order to identify at an early stage any possible need for action following a critical reflection of the results.

In addition to the standard stress tests carried out as part of the risk-bearing capacity assessment, the Group conducts an inverse stress test once a year. Inverse stress tests assess the level of severity at which specific stress factors could threaten the grenke Group’s continued existence.

Liquidity position

The Internal Liquidity Adequacy Assessment Process (ILAAP) is intended to ensure that the Group maintains adequate liquidity and sufficient refinancing options at all times within a defined time horizon. In the analyses, a distinction is made between the normative and economic perspectives to provide a comprehensive assessment of the grenke Group’s liquidity position and solvency.

The normative perspective of the ILAAP serves to ensure compliance with regulatory liquidity requirements over the planning horizon, taking into account business planning and stress scenarios. It focuses specifically on compliance with the regulatory liquidity ratios, liquidity coverage ratio (LCR) and net stable funding ratio (NSFR). The LCR is defined as the ratio of the available pool of liquid assets (liquidity buffer) to net liquidity outflows under defined stress conditions over the next 30 days. The NSFR sets the available amount of stable refinancing (own funds and liabilities) in relation to the required amount of stable refinancing (lending business). The refinancing sources, or assets, are weighted using supervisory-defined weighting factors based on their degree of stability.

The economic perspective of the ILAAP assesses the institution’s liquidity risk-bearing capacity by analysing whether sufficient liquidity reserves are available to ensure solvency, even under defined stress scenarios. The assessment is carried out independently of regulatory minimum requirements and serves internal management purposes.

Risk reporting

A key element of the risk management process is comprehensive, standardised internal and external risk reporting. Corporate Risk Management prepares a quarterly risk report for the Board of Directors, the Supervisory Board and key decision-makers (risk owners) of the Company, analysing and monitoring the current risk situation at Group level. The report covers the ICAAP and ILAAP results as at the reporting date, developments in the volume and structure of new business, developments across the individual risk types and, in particular, changes in the key regulatory and economic risk metrics together with the related early warning indicators. These provide insight into compliance with the risk appetite and, where applicable, the need for additional management action.

The key risk indicators and the liquidity position, including the ILAAP, are also monitored and reported monthly to the Board of Directors and the relevant risk owners. Internal ad hoc risk reports are also prepared in specific risk situations. A further element of the enhanced risk management is a recovery plan required as standard under supervisory regulation. It is based on the key risk (early) warning indicators and is closely embedded within the governance and ongoing risk monitoring and management processes. This enables grenke to respond quickly and in a focused manner to potential crisis situations, thereby strengthening its resilience.

Material risk types

The following section explains in greater detail the origin of the material risks in the context of grenke’s business model and sets out how these risks are measured and managed within the risk management framework.

Credit risks

The grenke Group’s strategic focus is on small-ticket leasing in the B2B segment, primarily serving small and medium-sized enterprises (SMEs), self-employed professionals and commercial enterprises. Although smaller companies represent the preferred target group, contracts are also entered into with larger customers that exceed the SME criteria (number of employees, revenue and total assets). As a result of the predominantly small-ticket business conducted in 31 countries, the portfolio is highly diversified from a risk perspective. In the small-ticket leasing segment, the contracts are characterised by low acquisition values up to EUR 50,000. This segment accounted for 96.5 percent (previous year: 97.1 percent) of all lease contracts during the reporting year.

Credit risks arise predominantly from the core leasing business and include, in particular, default risk and migration risk. Default risk describes the risk that a customer is unable to meet its payment obligations under leasing contracts. Migration risk reflects changes in value that may arise from a change in the credit rating classification (rating migration) of a borrower or lessee. Both sub-types of risk have been assessed as material in the risk inventory due to their potential impact on the net assets and results of operations.

To assess default risk, an internally developed, largely country-specific application scoring system is used prior to entering into a leasing contract. This incorporates information from credit agencies as well as other customer-specific and contract-specific characteristics. The models used by the Group generate a forecast, or expected value, of future default losses. These are incorporated as risk costs in the contribution margin calculation. The contribution margin calculation aggregates expected earnings components (operating income after risk) for each leasing contract and serves as a key basis for the contract decision. Across the Group, the aim when entering into lease contracts is to achieve the broadest possible portfolio diversification in order to spread risk.

For the receivables portfolio, expected losses from default risks arising from the leasing, factoring and lending business are also determined on the basis of internally developed risk models and backed with appropriate risk provisions in accordance with IFRS 9. In addition, expected losses on non-performing exposures are taken into account through standardised specific valuation allowances.

The regulatory capital requirement for credit risks (minimum capital requirements under Pillar I in accordance with the CRR) is determined on the basis of the Standardised Approach to Credit Risk (KSA). For the calculation of unexpected losses from performing receivables within the economic perspective of the risk-bearing capacity assessment, grenke uses a model based on the Gordy formula. For the non-performing portfolio, a model aligned with the requirements of the internal ratings-based approach (IRBA) is used to reflect the risk of losses exceeding the recognised best estimates.

Migration risk, which has also been classified as material, is taken into account not only through the recognition of credit deterioration via the IFRS 9 levels in determining risk provisions, but in particular within stress calculations through the application of historically increased risk parameters.

Market price risks

Market price risks refer to potential losses that may arise from uncertainty regarding the future development (level and volatility) of market risk parameters. Within the risk inventory, interest rate risk, currency risk and credit spread risk were classified as material risk sub-types.

Open interest rate and currency positions are entered into only in connection with the operating business and within economically required limits. In specific situations, derivatives are also used in a targeted manner in this context. Where possible and appropriate, the grenke Group uses derivative financial instruments in a targeted manner to reduce or eliminate risks arising from its ordinary business activities. Only interest rate swaps, currency swaps and foreign exchange forward transactions are used. Each derivative contract has an underlying economic transaction with a corresponding contrarian risk position. Contractual counterparties are credit institutions with predominantly good or very good credit quality and an S&P rating of BBB+ or higher. Further details on market price risks and, particularly, interest rate and currency risk management are provided in Chapter 7.3 Derivative Financial Instruments of the notes to the consolidated financial statements.

Interest rate risks

The Group’s interest rate risks arise from changes in market interest rate levels affecting all interest-bearing balance sheet positions and the resulting impact on net interest income. The grenke Group does not engage in active maturity transformation, but instead pursues a maturity-matched financing strategy in order to limit, as far as possible, risks arising from changes in market interest rates and refinancing risks.

Interest rate risk is measured within the risk-bearing capacity framework using a historical simulation with a 12-month risk horizon and a confidence level of 99.9 percent.

In addition, interest rate risk is assessed using interest rate shock scenarios in accordance with the requirements of BaFin and the European Banking Authority (EBA), and is analysed from both a present value perspective and a periodic earnings perspective. The present value analysis is performed using the economic value of equity (EVE) method, while the impact on periodic profit is assessed using the net interest income (NII) perspective.

Operational responsibility for monitoring and managing market price risks lies with the Treasury function. By adhering to the risk-strategic principle of avoiding significant maturity transformation, overall market price risks are maintained at a relatively low level. Market price risks (interest rate and currency risks) are also limited on the basis of risk limits approved by the Board of Directors within the risk-bearing capacity framework.

Currency risks

As a result of the international nature of its business, the grenke Group is exposed to currency risks. To limit or eliminate these risks, internally defined hedging strategies are applied. The derivatives used are recognised in the balance sheet at their market values as at the reporting date under financial assets or financial liabilities. Where possible, we refinance acquired new business in the respective local currency. For example, in our largest foreign currency market, the United Kingdom, we have GBP refinancing. We also have BRL financing in Brazil, and the AUD bond issued for the first time last year underlines this ambition. This reflects the fact that our subsidiaries generally conduct their operating business in their respective local markets rather than across national borders (cross-border). In certain foreign currency regions, however, we use refinancing options in EUR, which are transferred into the respective local currency through intra-Group transactions and, where economically appropriate, hedged against exchange rate fluctuations using derivatives.

The risk arising from open currency positions is calculated within the risk-bearing capacity framework using a historical simulation of the relevant exchange rates as risk parameters, with a 12-month risk horizon and a confidence level of 99.9 percent.

Risks arise primarily from currency fluctuations related to financial assets or receivables and pending foreign currency transactions, as well as from foreign currency translation in the consolidation of Group entities. The use of derivatives – in the foreign currency area, foreign exchange forward transactions and currency swaps – counteracts the market sensitivity of the underlying transactions, i.e. the cash flows from financial assets or receivables. Ideally, this results in an almost complete hedge.

Further currency risks exist primarily in the area of financing for Group entities operating outside the eurozone. Open foreign currency cash flows are hedged on the basis of internally defined hedging limits, which apply once positions reach the equivalent of EUR 500 thousand per currency at the daily exchange rate. Foreign exchange forward transactions in particular serve as a key management instrument in this context.

Currency risks arising from the cash flows of issued foreign currency bonds are hedged by entering into maturity-matched cross-currency swaps.

Credit spread risk

Credit spread risk in the banking book (CSRBB) comprises risks arising from market-wide movements in credit spreads (including market liquidity spreads), excluding idiosyncratic components or creditworthiness-driven changes (e.g. rating migration). Rising credit spreads increase grenke’s costs for new capital market issues and can only be reflected in the terms and conditions of the leasing new business with a time lag. As a result, this risk type is also taken into account within the adverse scenarios of capital planning.

For CSRBB, fluctuations in the segment- and rating-specific credit spread curve (non-bank financial segment, rating BBB) are considered as the relevant risk factor. The credit spread curve shows the credit premium (spread) on bonds issued by non-bank financial institutions with a BBB rating compared with risk-free yields across different maturities. Changes in the spread curve are not driven by rating changes of the issuers but instead reflect market-wide factors relevant under the CSRBB framework requirements.

Liquidity risks

Liquidity risks refer to potential losses that may arise if liquid funds are unavailable or can only be obtained at a higher cost than expected to meet payment obligations when due. Material sub-types include liquidity risk in the narrower sense, i.e. the risk that current and future payment obligations cannot be met in full or on time, and refinancing risk, i.e. the risk that refinancing at the required time can only be obtained on more expensive terms than expected.

Liquidity risks may arise from all positions entered into with external parties. The grenke Group’s refinancing sources consist primarily of ABCP programmes, bond and promissory note issuances, the deposit business of grenke Bank AG, a syndicated credit facility with a banking consortium and the issuance of subordinated bonds (hybrid capital).

Liquidity risks at the grenke Group are limited through compliance with the regulatory ratios LCR and NSFR. The objective is to achieve alignment between balance sheet assets and liabilities, primarily measured by duration, and the broadest possible diversification of refinancing sources. Concentration risks in refinancing are reduced to an economically reasonable level.

As with market price risks, liquidity risks are mitigated overall by the principle of avoiding significant maturity transformation. Liquidity risks are managed operationally by the Treasury department, overseen strategically by management and monitored by Corporate Risk Management. At Group level, liquidity risk is managed, among other measures, through weekly liquidity overviews (e.g. LCR and NSFR) and monthly dynamic liquidity and refinancing planning. Three stress scenarios (institution-specific, market-specific and combined) are typically analysed. Surplus liquidity is invested in accordance with, and within the framework of, the approved counterparty limits.

Short-term liquidity

Liquidity risk management includes the daily management of cash inflows and outflows. For short-term reporting purposes, a liquidity overview is prepared on the first working day of each calendar week and reviewed at Board of Directors level. It contains all relevant information on short-term liquidity developments over the coming weeks. The weekly liquidity overview presents the Group’s current liquidity position. The focus is on cash flows from the leasing business. Wage and tax payments are also taken into account.

The reporting distinguishes between three liquidity levels:

- Liquidity 1 (cash liquidity): funds held in all accounts plus available bank overdraft facilities and all funds that are “immediately” available (time horizon of approximately one week).

- Liquidity 2: Liquidity 2 comprises Liquidity 1 plus funds due or expected to be received within one month, as well as encumbered assets that can be monetised within one month without significant loss of value.

- Liquidity 3: Liquidity 3 comprises Liquidity 2 plus funds not due or expected to be received within one month, together with invested assets that require more than one month to be monetised without significant loss of value.

EURk

Dec. 31, 2025

Dec. 31, 2024

Liquidity 1 (cash liquidity)

466,640

446,922

Liquidity 2 (up to 4 weeks)

260,513

87,424

Liquidity 3 (more than 4 weeks)

704,799

888,717

Medium and long-term liquidity

In addition to short-term liquidity management and weekly reporting, a static liquidity plan is prepared each month. This planning is based on the assumption that the existing lease, lending and factoring portfolios are liquidated according to the terms of the contractual agreements, such as that funds from the assets are received when due. Liabilities are also repaid when due in accordance with the contractual agreements in place. Since the duration of the liabilities side (liabilities) approximately corresponds to that of the portfolio, largely maturity-matched financing is ensured. In this context, reference is also made to the overview of expected cash outflows from contractual obligations in Section 2.7.3 “Liquidity”.

Liquidity development

Liquidity development

In addition, a dynamic liquidity plan is prepared each month. It aims to reflect the liquidity position under stress conditions and thus liquidity risk in the narrower sense for the coming periods, and serves to manage the Group’s overall liquidity position. Refinancing risk is assessed at least quarterly as part of the risk-bearing capacity assessment. This includes examining whether, and to what extent, an increase in credit spreads leads to higher refinancing costs and thus increases refinancing risk.

Operational risks

Operational risk is the risk of losses resulting from inadequate or failed internal processes, people and systems, or from external events. This definition includes legal risks, while strategic and reputational risks are not included.

Operational risks (in accordance with the CRR) arise in particular from external fraudulent acts, human error, physical hazards, inadequate internal regulations and internal fraudulent acts. This sub-type of risk has been assessed as material within the framework of the risk inventory due to its potential impact on the net assets, results of operations and liquidity position.

Conduct risks arise from the inappropriate provision of financial services in the areas of leasing, banking and factoring, as well as from issues relating to customers, products and business practices, and from internal fraudulent acts and human error. Compliance risks arise, among other factors, from inadequate internal regulations. These two sub-types of risk have been assessed as material in the risk inventory due to their potential impact on the net assets, results of operations and liquidity position.

Model risks may arise from errors in the development, implementation or use of models. Model risks have been assessed as material due to their impact on the net assets and results of operations.

Information and communication technology (ICT) risks and information security risks arise for grenke from cyberattacks, technical failures or errors, as well as from human error and inadequate internal regulations. The sub-types of ICT risk have been assessed as material in the risk inventory, in particular due to their potential impact on the net assets and results of operations.

Human capital risks, particularly those arising from staffing shortages, staff turnover or inadequate qualifications, are not managed as a separate risk category but are considered as part of operational risk.

Operational risks are limited through risk limits within the risk-bearing capacity model. Regular quantification within the risk-bearing capacity calculation is currently performed using the standardised approach under Basel IV as the base model, including a component that incorporates institution-specific loss data. For the purpose of determining the total capital ratio under CRR III at Group level, operational risk is calculated using the new supervisory harmonised standardised approach. In addition, specific manifestations of ICT risk are assessed quarterly and reported as part of risk reporting. While legal and compliance risks are already taken into account through the internal risk-bearing capacity model, model risk is considered separately within the risk-bearing capacity calculation. Model risk is recognised in the form of a risk buffer derived from the risk inventory.

For the Group-wide monitoring of operational risks, grenke has implemented indicators (e.g. cost and organisational indicators). In addition, all fraud cases and other operational loss events are recorded and analysed in a loss event database. To enable the early identification of management measures, the volume of operational loss events is monitored against defined thresholds. In connection with human capital risks, staff turnover is regularly monitored as an indicator. A Group-wide compliance management system monitors the diverse international requirements, and all employees receive regular information and training through awareness measures.

In addition to the annual risk inventory and the ongoing reporting of losses and risks, the annual OpRisk self-assessment contributes to the identification of operational risks. The objective of the operational risk management process is to mitigate loss potential while maintaining business operations and at the same time optimising the use and protection of assets.

Business process and IT risk management

All core business, management and support processes of the grenke Group are aligned with the business strategy and standardised and digitalised. They are enhanced on an ongoing basis to simplify them and increase their efficiency. This requires a technologically modern and highly flexible system architecture, the modification of which (change management) is systematically documented in terms of content and methodology and subject to regular review. A high level of operational stability is achieved through the continuous modernisation of the infrastructure, based on a fully redundant data centre architecture. The development of a suitable multi-cloud infrastructure, initiated in 2023, was largely completed in 2025, and parts of the IT landscape were migrated to the cloud. IT risk management ensures full risk transparency across all IT functional areas, including organisation, processes, applications, infrastructure operations (including IT security), projects and compliance.

Cyber and ICT risks are measured and managed on the basis of information networks, which are structured around grenke-specific business process clusters. These are supplemented with additional IT-specific information, such as the applications used or hardware components. As a result, the measured ICT and cyber risk relates to the material business processes and provides a reliable assessment of the quality of service support delivered by the Group’s ICT systems. In the reporting year, the relevant ICT and cyber risks were identified as part of the risk inventory. Despite existing latent risks, the performance of the Group’s ICT systems is considered adequate overall. The identified findings are being addressed through ongoing projects.

Business continuity management

In 2025, grenke further enhanced its business continuity management (BCM), thereby reinforcing the Company’s operational resilience on a sustainable basis. The focus was on strengthening the organisation’s resilience, incorporating regulatory requirements at an early stage and further developing an effective and reliable business continuity management system (BCMS).

During the reporting year, the Business Continuity Management team further strengthened its role in the implementation of regulatory and strategic initiatives. In this context, BCM plays a key role in identifying critical or important functions and strengthening operational resilience. During the reporting year, BCM reporting was aligned with the principles of ISO 22301.

Another key achievement during the reporting year was strengthening BCM governance and its supporting management mechanisms. Uniform requirements, aligned policies and clearly defined responsibilities enhanced transparency and reliability. Close coordination with the Information Security, IT and Corporate Risk Management departments supported an integrated management approach that holistically safeguards critical or important functions and provides a sound basis for decision-making.

grenke further refined its business impact analysis (BIA) and presented it in a transparent manner. A consistent methodology, a more precise classification of critical or important functions and a clear presentation of dependencies created a reliable foundation for transparency and consistent application across grenke, particularly in managing emergencies and crisis situations. Additional internal communication measures and training materials fostered a shared understanding across the relevant organisational units.

To further strengthen resilience, grenke systematically updated emergency and test scenarios and integrated them into the existing emergency framework. During the reporting year, grenke used insights from external events, including large-scale supply disruptions in Europe (e.g. power outages on the Iberian Peninsula), as well as internal analyses, to further enhance emergency preparedness.

Building on this, grenke introduced new and enhanced templates for business continuity plans, as well as ICT-related response and recovery plans and supported their introduction through communication and training measures. grenke continues to develop its existing emergency plans to further strengthen the organisation’s ability to respond effectively in crisis situations.

The digitalisation and system support of the Business Continuity Management team was also increased. A central tool facilitates the consistent, convenient documentation of the BIA as well as emergency and crisis prepared-

ness. The test phase carried out during the reporting year improved the day-to-day application, firmly embedding the digital BCM framework within the organisation.

In 2026, grenke intends to continue to move forward with the BCM’s digital transformation. The BCM tool will move into full operational use and provide comprehensive support across all BCM processes. This will increase transparency, enhance oversight and promote effective collaboration across organisational units. Another key focus is the ongoing development of employee awareness. grenke is refining and broadening its training and communication formats to reinforce a sustainable awareness of business continuity, emergency preparedness and crisis management. At the same time, the Company is advancing its crisis management to further enhance its ability to respond effectively in complex and fast-moving situations. In 2026, grenke also plans to refine the emergency testing concept and to continue enhancing emergency exercises and resilience testing to review and improve preparedness.

Business and strategic risk arise when earnings develop unexpectedly and are not covered by other risk categories. This includes risks arising from changes in key framework conditions (e.g. the economic and product environment, legislative changes related to sustainability, customer behaviour and the competitive landscape) and losses resulting from inadequate strategic positioning. The Group considers these risks material.

The grenke Group’s entrepreneurial success depends to a significant extent on the success of its sales activities within the targeted sales channels. The risk of failing to achieve sales targets arises if sales performance does not develop as expected due to internal or external factors, causing the assumptions underlying sales planning (leasing new business assumptions) to deviate from expectations.

Within the economic risk-bearing capacity framework, grenke applies the earnings at risk (EaR) approach as its central modelling concept. Under this method, it analyses empirical plan–actual deviations of selected income statement items based on financial years and aggregates them into a sufficiently conservative risk metric.

In a dynamic market environment, it is important to anticipate changes at an early stage and take timely action to adapt to new market conditions and limit potential risks. grenke AG continuously monitors exogenous market influences and the risks arising from them.

Reputational risk arises when damage to the Company’s reputation or standing leads to adverse effects on key metrics such as earnings, own funds, liquidity and the share price. The grenke Group considers reputational risks to be material.

Reputational risk is of particular importance. For grenke as a capital market-oriented company, an impeccable reputation is particularly relevant, inter alia, with regard to its market position and refinancing opportunities.

Within the risk-bearing capacity calculation, reputational risks are taken into account by means of a flat-rate risk buffer, which is derived from the risk inventory.

The management of reputational risk is carried out primarily through forward-looking and sustainable corporate governance and adequate risk management, which are supported by solid governance structures and transparent corporate communication.

Other risks include and consider pension risk, insurance risk, real estate risk, investment risk, step-in risk, sovereign risk and tax risk, in addition to risks arising from changes in the legal, political and social environments.

Of the sub-types of other risks, tax risk was classified as material to the results of operations as part of the current risk inventory. It particularly includes risks arising from changes in tax regulations as well as from differing tax assessments by tax authorities. Potential impacts may be reflected in additional tax expenses or subsequent payments. Tax risk is taken into account within the normative perspective of the risk-bearing capacity calculation.

The other risk types and risk sub-types under the category “Other risks” are considered immaterial risk sub-types.

The process for analysing risks classified as immaterial in the risk inventory is supplemented by an aggregate assessment including all downstream entities with regard to risks that are immaterial when considered individually. In addition, a review of the materiality of the sum of all individually immaterial risks is included.

In a dynamic market environment, it is important to identify changes at an early stage and to take timely measures to adapt to new market conditions and to limit potential risks. grenke therefore monitors exogenous market influences and the risks that may arise from them. With the establishment and continuous further development of the risk inventory and the early warning indicator set, other risks within the Group in particular are identified, assessed and monitored according to a uniform pattern.

ESG risks

ESG risks encompass a wide range of aspects. In the areas of climate and environment (Environmental), ESG risks are divided into physical risks and transitional risks. Physical risks relate to the direct effects of climate change and environmental pollution, such as floods, droughts and other extreme weather events (acute physical risks). However, they may also arise from long-term changes in climatic and economic conditions (chronic physical risks). Physical risks may also have indirect consequences. Transitional risks, by contrast, are risks that may arise, for example, from politically motivated changes or changes in consumer behaviour. Social risks (Social) concern the social aspects of corporate governance and may include both internal aspects such as working conditions and employee motivation, as well as external factors such as relationships with customers, suppliers and the local community. Topics such as human rights, occupational health and safety, diversity and inclusion, as well as responsibility in the supply chain play a central role here. Governance risks (Governance) concern the way in which a company is managed and include aspects such as transparency, ethical business practices, corruption prevention, accountability of executives, as well as the independence and integrity of the Supervisory Board.

The grenke Group considers ESG risks to be a sub-aspect of the known risk types. Consequently, ESG risks are not defined as an isolated risk type in the risk catalogue for the risk inventory. ESG risks affect various risk types. In addition to their current impact, their future effects are also considered across different time horizons.

As part of the risk inventory, ESG risks are qualitatively assessed as risk drivers for the respective risk types, and a heat map is prepared to illustrate how their impact develops over time. At present, ESG risks are identified as having an impact on all risk types. Climate and environmental risks in particular are expected to increase over time and to be classified as material in the long term. To further analyse the impact of ESG risks, an additional assessment was conducted based on the ESG score. The ESG score functions as an internal scoring model for evaluating ESG risks in the volume business. Based on this scoring model, regular portfolio clustering can be performed, which in turn enables ongoing change analyses and more detailed risk analyses, particularly in peripheral areas. Scores can be aggregated at sub-portfolio level, for example by sector and by country. Individual risk driver scores (E-physical, E-transitional, S and G) also allow for clear differentiation. The assessment of physical risks explicitly incorporates scientific forward-looking analyses.

In addition, ESG risks are reflected in stress testing calculations within both the economic and normative perspectives of risk-bearing capacity in relation to capital. Integrating ESG risks into the risk control process represents a key step in addressing the growing importance of sustainability and responsible business practices. The ongoing refinement of risk management processes, together with close cooperation between the relevant departments and management, ensures that ESG risks are properly embedded in the long-term corporate strategy.

Development of the risk landscape

Risk-bearing capacity in the normative perspective was consistently ensured in the grenke Group in the 2025 financial year. At each risk reporting date, capital ratios exceeded the regulatory capital requirements.

Compared with the previous year, both the Common Equity Tier 1 ratio and the total capital ratio declined as of December 31, 2025. The total capital ratio under CRR stood at 15.2 percent on the reporting date (previous year: 17.4 percent), while the CET1 ratio was 12.4 percent (previous year: 14.4 percent). The main drivers of this development were the strong growth in new business, resulting in a rise in risk-weighted assets (RWA), and further effects from M&A transactions successfully completed in 2025.

In addition to the risk-adjusted capital requirement, the CRR also requires compliance with a leverage ratio, which is largely based on balance sheet metrics and is therefore not risk-sensitive. As of the reporting date, the leverage ratio pursuant to Art. 429 CRR was 12.5 percent (previous year: 14.3 percent). The minimum ratio of 3.0 percent required by the supervisory authorities as of the reporting date was therefore met.

The following table shows the composition of Tier 1 capital, the total own funds, and the relevant risk positions as of the reporting date, December 31, 2025.

EURk

Dec. 31, 2025

Dec. 31, 2024

Paid-in capital instruments

46,496

46,496

Premium on capital stock

298,019

298,019

Retained earnings

783,933

773,400

Other comprehensive income

9,215

4,499

Deductions from core capital

– 247,380

– 154,802

Transitional provisions pursuant to Section 478 CRR

-

-

Total Tier 1 capital pursuant to Section 26 CRR

890,283

967,612

Total additional core capital pursuant to Section 51 CRR

200,000

200,000

Total supplementary capital pursuant to Section 62 CRR

Total equity pursuant to section 25 ff CRR

1,090,283

1,167,612

EURk

Dec. 31, 2025

Dec. 31, 2024

Equity requirements for credit risk with central governments and central banks

-

-

Equity requirements for credit risk with regional / local authorities

7,017

7,687

Equity requirements for credit risk with institutions /

corporations with short-term rating

8,119

9,791

Equity requirements for credit risk with corporations

310,282

268,544

Equity requirements for credit risk from retail business

135,494

124,637

Equity requirements for credit risk from other positions

31,455

17,283

Equity requirements for credit risk from investments

228

236

Equity requirements for credit risk from subordinated debt exposures

1,979

-

Equity requirements for credit risk from non-performing positions

32,347

27,690

Total equity requirements for credit risk

526,921

455,869

Total equity requirements for market risk

-

-

Total equity requirements for operational risk

46,198

80,411

Total equity requirements for credit valuation adjustments

1,501

1,720

Total equity requirements

574,619

538,000

Risk-bearing capacity in the economic perspective was consistently ensured in the grenke Group in the 2025 financial year.

The risk coverage potential of the grenke Group in the economic perspective amounts to EUR 2,295 million as of the reporting date of December 31, 2025 (previous year: EUR 2,299 million). Of this amount, a total of EUR 1,565 million (previous year: EUR 1,509 million) is allocated as risk capital in the form of limits to the material risk types as of December 31, 2025. The limits resolved by the Management Board within the framework of the economic perspective were complied with at every reporting date.

As of December 31, 2025

in EUR million

Utilisation

in %

Risk coverage potential

2,295.4

Risk limit

1,565.0

68.0%

Risk

1,029.6

66.0%

in EUR million

Utilisation

in %

Credit risk

766.9

65.5%

Market risk

74.2

53.0%

Operational risk

78.3

65.2%

Business and strategic risk (lump-sum risk buffer)

65.2

72.4%

Reputational risk

(lump-sum risk buffer)

45.0

In the risk-bearing capacity calculation, the present value of the total risk of the grenke Group at a confidence level of 99.9 percent amounts to approximately EUR 1,030 million as of December 31, 2025 (previous year: EUR 1,001 million). This results in a limit utilisation of 66 percent as of the reporting date (previous year: 66 percent). The overall risk utilisation of permanently below 95 percent specified in the Group’s risk strategy valid as of the reporting date was therefore complied with.

As in the previous year, as of December 31, 2025, there were no risks whose occurrence would jeopardise the existence of the Group or a significant Group company. With regard to the future development of the Group and the Company as well as its subsidiaries, no particular risks exceeding the normal level and associated with the business are identifiable.

Credit risks

The unexpected loss from credit risks amounts to approximately EUR 767 million as of the reporting date (previous year: EUR 743 million). The utilisation of the risk limit amounted to 66 percent (previous year: 65 percent). The increase in risk compared to the previous year is primarily due to the higher receivables volume resulting from new business growth.

grenke Group

The receivables volume of the grenke Group amounted to a total of EUR 8.3 billion as of December 31, 2025 (previous year: EUR 7.7 billion), With approximately EUR 7.3 billion (previous year: EUR 6.5 billion), the vast majority of the receivables volume related to current and non-current lease receivables.

EURk

Dec. 31, 2025

Dec. 31, 2024

Current receivables

Cash and cash equivalents

674,092

974,551

Lease receivables

2,489,734

2,594,088

Financial instruments with positive fair value

4,884

4,555

Other current financial assets

159,222

102,012

Trade receivables

10,758

9,706

Total current receivables

3,338,691

3,684,912

Non-current receivables

Lease receivables

4,852,193

3,922,154

Other non-current financial assets

63,803

79,776

Financial instruments with positive fair value

3,316

12,969

Investments accounted for using the equity method

2,053

2,444

Total non-current receivables

4,921,366

4,017,342

Total receivables volume

8,260,057

7,702,255

As of December 31, 2025, cash and cash equivalents included a balance with the Deutsche Bundesbank in the amount of EUR 549.2 million (previous year: EUR 790.7 million). The other cash and cash equivalents comprised – with the exception of EUR 12.1k cash on hand (previous year: EUR 6.9k) –

balances with domestic and foreign banks.

The financial instruments with positive market value represented the derivatives of the Group measured at fair value as of the reporting date.

The expected default losses for the 2025 new business portfolio of the grenke Group amounted to an average of 6.2 percent (previous year: 6.0 percent), based on the acquisition costs of the leased assets and over the entire contract term of an average of 49 months (previous year: 49 months).

The distribution of new business of the grenke Group (excluding receivables from the factoring business) by size categories is shown in the following table.

Percent

Dec. 31, 2025

Dec. 31, 2024

EURk <2.5

3.94

4.07

EURk 2.5–5

11.02

11.78

EURk 5–12.5

19.52

20.04

EURk 12.5–25

17.58

18.10

EURk 25–50

15.53

16.24

EURk 50–100

14.32

14.13

EURk 100–250

12.49

11.34

EURk >250

5.60

4.30

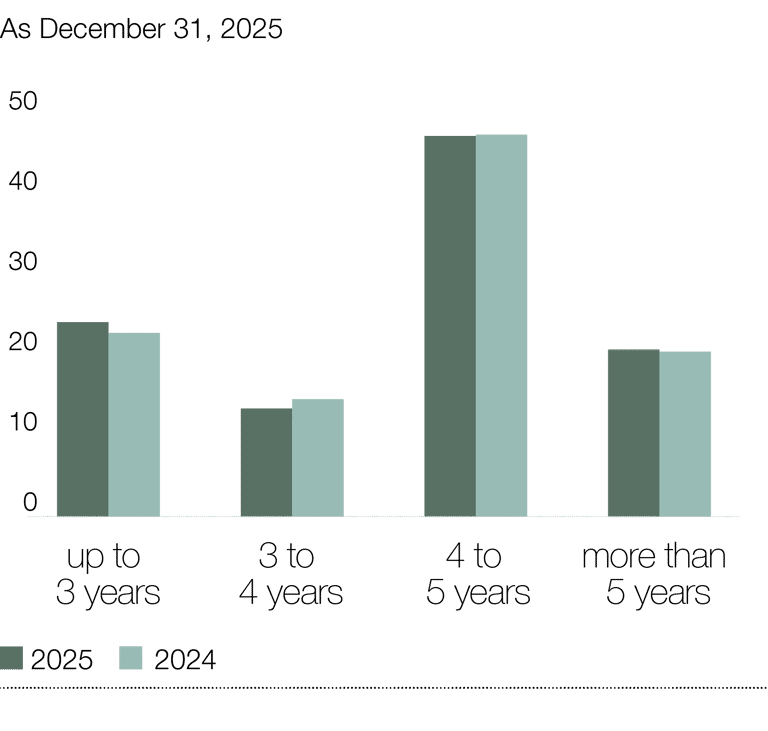

The receivables from the factoring business are entirely short-term in nature, therefore only the new business receivables from the Leasing and Banking segments are broken down by maturity class. The average contract term of the new business contracted in the reporting year remained unchanged year-on-year at 49 months.

Leasing new business by maturity category

As of December 31, 2025, lease receivables accounted for 89 percent of the grenke Group’s total receivables volume (previous year: 85 percent). The Group therefore regards the credit default risk of its leasing customers as its most significant risk. As of December 31, 2025, the portfolio was concentrated in the top 6 countries – Germany, Finland, France, the United Kingdom, Italy and Spain – which together account for 71 percent of the total lease receivables volume.

To determine the risk provisions for lease receivables in accordance with IFRS 9, lease receivables are allocated to three levels depending on their respective credit risk. Impairments for Level 1 lease contracts correspond to the expected loss over a twelve-month period. For lease receivables in Level 2, a risk provision is recognised for the expected loss over the remaining contract term. For lease receivables in Level 3, expected losses are recognised as risk provisions. The total addition to risk provisions at the Consolidated Group level for the leasing business amounted to EUR 194.5 million in the 2025 financial year.

grenke Bank

By purchasing intra-Group lease receivables, grenke Bank AG constitutes a key pillar of the grenke Group’s refinancing strategy. In addition, intra-group refinancing is conducted for subsidiaries of the grenke Group. receivables arising from the lending business of grenke Bank AG consist primarily of microcredit and the Bank’s own SME business. Credit default risk represents the principal risk for grenke Bank AG.

Intra-group leasing purchases constitute by far the largest portion of the Bank’s customer business, accounting for approximately 87.3 percent and a risk volume of EUR 2,069 million. Intra-group refinancing of companies within the grenke Group amounts to a risk volume of EUR 70.1 million. In cooperation with the Mikrokreditfonds Deutschland and selected microfinance institutions, grenke Bank AG has been granting microloans of up to EUR 25k to SMEs since 2015. The processing and refinancing are carried out on behalf of the Federal Republic of Germany. The credit default risk is fully borne by the Mikrokreditfonds Deutschland. As of the end of 2025, grenke Bank AG’s receivables from the microcredit business amounted to EUR 92.4 million (previous year: EUR 91.3 million). As a financing partner for SMEs, grenke Bank AG also provides loans and overdraft facilities on its own account for SMEs. The risk volume of grenke Bank AG from its SME lending business amounted to EUR 68.0 million at year-end 2025 (previous year: EUR 51.0 million). grenke Bank AG’s lending business also focuses on the small-ticket segment, with the average receivables volume per customer standing at EUR 15.2k as of December 31, 2025 (previous year: EUR 12.7k).

The calculation of risk provisions for receivables arising from the lending business of grenke Bank AG is based on an individual assessment and determination of a specific loss allowance for each exposure. In 2025, grenke Bank was able to reverse EUR 0.5 million in risk provisions for the lending business. The year-on-year decrease was primarily attributable to the reversal of previously recognised loss allowances due to collection of payments and recoveries from impaired receivables, as well as to the write-up of a held investment.

Factoring business

The grenke Group’s factoring business also focuses on the small-ticket segment. In addition to its own subsidiaries in Germany, the United Kingdom, Ireland, and Hungary, branches of grenke Bank in Italy and Portugal provide factoring services. The Consolidated Group’s factoring units primarily handle factoring contracts with domestic debtors. The main service offered is notification factoring, where invoice recipients (debtors) are informed of the assignment of receivables. Under certain conditions, non-notification factoring is also offered, where the debtor is not informed about the assignment of receivables to the factoring company. Additionally, the service portfolio includes “non-recourse factoring,” where the credit risk remains with the factoring clients. As of December 31, 2025, the total volume of factoring receivables across all entities amounted to EUR 87.48 million (previous year: EUR 103.41 million). The decline is attributable to the sale of the factoring company in Poland and to the discontinuation of operations of the factoring company in Switzerland.

As of December 31, 2025, the Consolidated Group’s factoring business had 13 customers with receivables exceeding EUR 1.0 million, accounting for 23.92 percent of total factoring receivables.

Impairments for expected losses from factoring receivables are recognised based on the 12-month expected credit loss. Since factoring receivables are short-term, the 12-month expected credit loss corresponds to the lifetime expected credit loss. As of December 31, 2025, the balance of impairments in the factoring business amounted to EUR 7.8 million (previous year: EUR 10.0 million). The reduction in risk provisions at the Consolidated Group level for the factoring business totalled EUR 2.2 million. This reduction also is largely due to the sale of the Polish company and the discontinuation of business activities of the factoring company in Switzerland.

grenke is divesting its entire factoring division. While the sale of the company in Poland has been completed, the companies in the United Kingdom, Ireland, Germany and Hungary, as well as the branches of grenke Bank in Italy and Portugal, will follow in 2026.

However, the sale of the companies in Germany and Hungary is still subject to approval by the respective supervisory authorities under the ownership control procedure.

Investments

As of the reporting date, the Consolidated Group holds a 13.7 percent stake in Munich-based Finanzchef24 GmbH through grenke Bank AG, which is included in the consolidated financial statements. In 2023, the Group acquired a minority interest of 26.0 percent in Miete24 P4Y GmbH.

Market price risk

The unexpected loss from market price risks is determined using a historical simulation with a confidence level of 99.9 percent and amounts to approximately EUR 74.2 million as of the reporting date (previous year: EUR 116 million). The utilisation of the risk limit amounted to 53 percent (previous year: 58 percent). Interest rate risk was EUR 72.4 million (previous year: EUR 114 million). As of the reporting date, the result of the regulatory standard interest rate shock for the economic value of equity (EVE) under a parallel increase in interest rates of 200 basis points was – 3.24 percent (previous year: – 5.18 percent), while a parallel decrease of 200 basis points resulted in an increase of +2.66 percent (previous year: +4.80 percent). From the net interest income (NII) perspective, net interest income would increase by +1.11 percent under a parallel interest rate shock of +200 basis points and decrease by –1.50 percent under a parallel shock of – 200 basis points.

The value-at-risk (VaR) calculation for currency risk at a 99.9 percent confidence level indicated a risk of EUR 1.8 million as of December 31, 2025 (previous year: EUR 1.5 million). Due to strict volume limits on foreign currency holdings and a historical focus on eurozone countries, currency risk remained low during the reporting year even amid significant exchange rate fluctuations. According to management’s assessment, the Consolidated Group is materially exposed primarily to exchange rate risk relating to the British pound (GBP), Australian dollar (AUD), Swiss franc (CHF), Swedish krona (SEK), Brazilian real (BRL) and Danish krone (DKK). The selection of these currencies was based both on potential impacts identified through analysis and the volume of lease receivables in the respective countries.

The table shows, from the Consolidated Group’s perspective, the sensitivity of a 10 percent appreciation or depreciation of the euro against the respective other currencies as of December 31, 2025 or during the reporting period and its impact on the annual result before income taxes.

EURk

2025

2024

Appreciation

Depreciation

Appreciation

Depreciation

GBP

– 1.477

1.481

– 801

798

AUD

– 721

708

– 84

904

CHF

– 70

70

194

– 194

SEK

– 466

555

36

47

BRL

– 674

674

50

– 50

DKK

342

– 173

746

– 597

The effect on the annual result before income taxes arises from changes in the fair values of monetary assets and liabilities, including foreign currency derivatives not designated as hedging instruments, as well as from actual cash flows that were partially or fully recognised in profit or loss during the reporting period and had to be translated into euros during consolidation. All other influencing factors, particularly interest rates, were held constant. The effects of forecasted sales and purchase transactions were not considered. The changes in the value of cross-currency swaps have no material impact on the annual result before income taxes, as these are accounted for as hedging instruments. The value changes of these swaps primarily affect the Consolidated Group’s equity directly.

Operational risk

Operational risks amounting to approximately EUR 78.3 million (previous year: EUR 54.7 million) result in a risk limit utilisation of 65 percent as of the reporting date (previous year: 68 percent). This includes a risk buffer for model risks of EUR 10 million (previous year: EUR 10 million).

In the 2025 reporting year, 23 risk notifications (previous year: 21) were submitted. Risk reports document incidents that have occurred but have not yet caused harm and carry potential risk. Risk notifications serve the systematic recording and analysis of potential loss events, increase transparency regarding the operational risk profile and support the further development of the internal control system as well as risk management measures.

Business and strategic risks

Business and strategic risks of approximately EUR 65.2 million (previous year: risk buffer of EUR 47 million) corresponded to risk limit utilisation of 72 percent at the reporting date.

Risk buffer

As of December 31, 2025, the risk buffer for reputational risks amounted to EUR 45 million (previous year: EUR 40 million).

As of December 31, 2025, the liquidity coverage ratio (LCR) stood at 240.5 percent (previous year: 343.7 percent). The LCR minimum requirement of 100 percent was met at all times during 2025.

The net stable funding ratio (NSFR) was 114.5 percent as of December 31, 2025 (previous year: 115.8 percent), remaining above the regulatory minimum requirement of 100 percent.

The focus of the economic perspective is on the liquidity gap analysis and the defined stress scenarios. The specified minimum survival horizon was consistently maintained throughout the 2025 reporting period.

In addition to the accounting-related control system, grenke has instruments, procedures and controls for all material processes to ensure their robustness, effectiveness and efficiency. The nature, scope and complexity of the material processes determine the nature and scope of the associated controls.

The internal control system (ICS) at grenke pursues primarily the following objectives:

- Robustness, effectiveness and efficiency of business processes

- Compliance with the legal regulations applicable to grenke

- Identification of risk areas and points of weakness

Controls have been implemented as part of the individual processes to reduce the identified risks. The design of the controls and their integration into the processes, as well as the operational implementation of the controls, are the key determinants of risk minimisation for the effectiveness of the ICS.

The ICS implemented at grenke takes into account the regulatory and statutory requirements for financial services institutions for an appropriate and effective internal control system and, specifically, the Minimum Requirements for Risk Management (MaRisk) established by the German Federal Financial Supervisory Authority (BaFin), the Banking Supervision Requirements for IT (BAIT) and other relevant pronouncements by international supervisory authorities.

The effectiveness and appropriateness of risk management in general and the ICS in particular are reviewed and assessed by grenke’s Internal Audit department in a risk-oriented and process-independent manner according to the requirements of MaRisk AT 4.4.3.

The specifications and requirements for the structure and scope of the ICS are developed at Consolidated Group level and transferred to individual companies where appropriate and possible. The principles for structural and procedural organisation, as well as the processes of grenke’s Group-wide ICS, are developed on a continuous basis.

The responsibility for the ICS lies with the Board of Directors, in accordance with Section 91 AktG.

Internal control system related to the Consolidated Group accounting process

At grenke, the internal control system and the risk management system are both interlinked with regard to group accounting. In the following, the term “ICS” is used when referring to the internal control system. ICS represents the entirety of the principles, procedures and measures introduced by the Company’s management that are aimed at the organisational implementation of the management’s decisions in the organisation and ensures

- the effectiveness and efficiency of business activities, including the protection of assets and the prevention and detection of losses to assets;

- the correctness and reliability of internal and external accounting; and

- compliance with the legal provisions relevant to the Company.

The Board of Directors bears overall responsibility for the accounting process at the Company and the Consolidated Group. All of the companies included in the annual financial statements and the consolidated financial statements are also a part of a defined management and reporting organisation process. The Consolidated Group’s accounting and consolidation are organised centrally. The posting of each country’s local entity transactions is centrally recorded and processed in accordance with mandatory schedules for generating qualitative and quantitative information. The cross-check principle generally applies.

The principles, structures, process organisation and accounting methods used by the ICS are documented in writing and updated at regular intervals.

The systems used for the group accounting process and the required IT infrastructure are regularly reviewed by the Internal Audit department with regard to the necessary security requirements. The same applies to the continuing development of the Consolidated Group’s accounting process, particularly with respect to new products, facts and revised legal regulations. External consultants are brought in if necessary. To ensure the quality of the Consolidated Group’s accounting, the employees involved are regularly trained on a demand-driven basis. The Supervisory Board is also involved in the control system and supervises the Consolidated Group-wide risk management system, including the internal control systems in the areas of audit, accounting and compliance. The Supervisory Board also reviews the contents of the non-financial statement. The Supervisory Board is supported by the Audit Committee, whose focus is to oversee internal and external accounting and the accounting process.

In view of the accounting process for the Company and the Consolidated Group, features of the ICS are considered to be significant when they are capable of materially influencing the accounting and general statement presented in the financial statements, including the combined management report. These features include the following elements in particular:

- Identification of significant risk and control areas relevant to the accounting process

- Controls to monitor the accounting process and its results at the levels of the Board of Directors and the companies included in the financial statements

- Preventative control measures in the finance and accounting systems as well as in the operative, performance-oriented company processes that generate material information for the preparation of the financial statements and the combined management report, and a separation of functions and predefined approval processes in relevant areas

- Measures that safeguard the orderly IT-based processing of accounting issues and data

- The establishment of an internal audit system to monitor accounting-related ICS

To reduce the identified risks, controls are implemented as part of the Group’s accounting process. For the effectiveness of the ICS, the design of the controls, their integration into the process, and the operational implementation are the important determinants of risk minimisation. Internal Audit regularly examines the ICS for the Consolidated Group’s accounting process in sub areas on a rotating basis, which reinforces the ICS.

As a financial holding company and parent of subsidiary institutions, the grenke Group is subject to a comprehensive regulatory framework. This framework requires the implementation of a proper business organisation supported by an appropriate and effective risk management system. The relevant regulatory requirements are defined in particular by the German Banking Act (Section 25a KWG) and the Minimum Requirements for Risk Management (MaRisk). In addition, the provisions of the Capital Requirements Regulation (CRR), including CRR II and CRR III, the Capital Requirements Directive (CRD V), and supplementary regulatory requirements apply at both Group and individual institution level.

As grenke AG qualifies as the superordinate undertaking of an institutional group as defined by sections 10a and 25a KWG, the grenke AG Group is classified as a financial holding company under the KWG pursuant to Section 1 (35) KWG in conjunction with Article 4 (1) No. 20 CRR. grenke AG also holds grenke Bank AG as a subsidiary credit institution. Both the grenke Group and grenke Bank AG are subject to the regulatory requirements of the Capital Requirements Regulation (CRR), as amended by CRR II and CRR III, as well as the Capital Requirements Directive (CRD V) and the KWG.

The grenke Group is required to implement the Minimum Requirements for Risk Management (MaRisk) and the Supervisory Requirements for IT (BAIT) issued by BaFin. These requirements consist of qualitative and quantitative standards for risk management that institutions must apply in line with their size and the nature, scope, complexity and risk profile of their business activities.

In addition, the financial services institutions GRENKEFACTORING GmbH and GRENKE Investitionen Verwaltungs KGaA are subject to the KWG and to supervision by BaFin and the Deutsche Bundesbank on an individual basis. For these entities, grenke AG makes use of the waiver provisions pursuant to Section 2a (1) or (2) in conjunction with Section 2a (5) KWG. Accordingly, these institutions have notified BaFin and the Deutsche Bundesbank that certain regulatory requirements are fulfilled at Group level rather than at individual institution level, as the necessary organisational arrangements are fully ensured by the superordinate institution. The application submitted by grenke AG to BaFin to align the regulatory scope of consolidation with the accounting scope of consolidation for Group financial reporting was approved in 2009. As a consequence, all entities attributable to the grenke Group are included in the regulatory scope of consolidation.

Furthermore, as the superordinate undertaking, grenke AG prepares a recovery plan in accordance with Section 12 (1) of the German Recovery and Resolution Act (SAG) at the request of BaFin. Recovery planning represents an industry-standard preventive measure involving the preparation of operational implementation plans for strategic planning, aimed at ensuring effective response options in the event of a potential crisis.

The Internal Capital Adequacy Assessment Process (ICAAP) is an internal company process designed on the basis of regulatory requirements to ensure on an ongoing basis that capital adequacy is maintained.